Behind the doors of French labs and pilot plants, researchers and manufacturers claim to have cracked one of the hardest parts of solid-state batteries: how to use ultra-thin lithium-metal layers without killing performance or safety. A new study, backed by big industrial names, is giving French “captains of industry” something they have lacked for years in this race — a clear technological roadmap.

France’s battery comeback starts with hard numbers, not hype

The timing matters. The global lithium-ion battery market is forecast to reach about €129 billion in 2026 and could surge towards nearly €479 billion by 2035, driven largely by electric vehicles and grid storage.

France fell behind during the initial surge of battery innovation especially in advanced chemical formulations. China South Korea & the United States moved forward rapidly during this period. Investment capital, skilled researchers and intellectual property accumulated in these foreign markets. Meanwhile French companies continued working primarily with traditional battery technologies. The gap widened as international competitors established strong positions in next-generation battery development. French industry maintained its focus on established methods rather than pursuing breakthrough innovations that were gaining traction elsewhere.

That picture is changing. Large-scale industrial programmes, new gigafactories, and public research that now works hand‑in‑hand with manufacturers are giving France a way back in. The hottest battleground is solid-state batteries, a technology many see as the “next generation” beyond today’s liquid-electrolyte lithium-ion cells.

France is shifting from talking about catching up to actually defining which technologies it wants to master, and at what cost and scale.

Why solid-state batteries are such a big deal

Most lithium-ion batteries today rely on a liquid electrolyte to function. This liquid allows lithium ions to travel back and forth between the positive and negative electrodes during charging and discharging cycles. However this design creates several significant drawbacks that affect both safety and performance. The liquid electrolyte poses serious safety concerns because it is highly flammable. If the battery gets damaged or overheats the liquid can ignite and cause fires. The liquid nature also means it can leak out of the battery over time or if the casing gets punctured. These risks force manufacturers to use heavy protective casings and add complex electronic monitoring systems to prevent dangerous situations. These safety requirements add weight and bulk to the battery. The thick protective layers take up space that could otherwise be used for energy storage. The monitoring electronics also add cost and complexity to the overall battery system. Beyond safety issues the liquid electrolyte limits battery performance in important ways. It restricts how quickly lithium ions can move through the battery which means slower charging speeds. The liquid also takes up volume without contributing to energy storage. This reduces the total amount of energy that can fit in a battery of a given size compared to what might be possible with other designs. All these limitations have pushed researchers to explore alternative electrolyte materials that could solve these problems while maintaining or improving the basic function of moving lithium ions between electrodes.

Solid-state batteries replace that liquid with a solid electrolyte. Think of it as a rigid membrane that lets ions through but cannot spill or burn. This change unlocks three major advantages: higher energy density, improved safety, and the ability to use lithium metal as the negative electrode.

Lithium metal is attractive because it stores far more energy per kilogram than the graphite used today in most EV batteries. In theory, that means longer driving ranges, smaller packs and much faster charging.

In practice, lithium metal is a headache. It forms dendrites — needle-like structures that can pierce the separator — and reacts easily with the electrolyte, creating dead layers that no longer store energy. Keeping it ultra-thin yet reliable is one of the hardest engineering problems in the field.

A new European defence giant is set to emerge outside Germany and France as the Czech-based Czechoslovak Group moves toward a landmark IPO. The company plans to list on the stock market in what could become one of the most significant defence industry public offerings in recent years. This development marks a shift in the European defence landscape as a major player emerges from Central Europe rather than the traditional powerhouses of Germany and France. Czechoslovak Group has grown substantially in recent years & now operates across multiple countries. The firm manufactures military equipment & provides defence services to various clients. Its decision to go public comes at a time when European nations are increasing their defence spending in response to regional security concerns. The IPO will give investors an opportunity to buy shares in a company that has established itself as a serious competitor in the European defence sector. Industry analysts expect strong interest from institutional investors who want exposure to the growing defence market. This move could reshape how people view the European defence industry. For decades Germany and France have dominated the sector with their large established companies. Now a Czech firm is positioning itself to join the top tier of European defence manufacturers. The timing appears strategic as governments across Europe are modernizing their military capabilities and seeking reliable suppliers. Czechoslovak Group has built a reputation for delivering quality products & maintaining strong relationships with defence ministries across the continent. The company’s leadership believes the public listing will provide capital for further expansion and help attract top talent. Going public will also increase transparency and potentially open doors to new government contracts that require publicly traded suppliers.

➡️ “I work in regulatory documentation and earn $70,100 a year”

➡️ Astrophysicists warn that the survival of a 13-billion-year-old signal challenges fundamental limits of cosmic information decay

➡️ A new study in Uganda shows chimpanzees applying insects to their wounds

➡️ This part of your washing machine isn’t dirty by accident: here’s what to do before it gets nasty

➡️ One bathroom product is enough: Rats won’t overwinter in your garden

# The 2026 China Car of the Year Is An Audi That Costs The Same As A Base A1 In France: The Gap Widens

The automotive industry continues to reveal stark differences between global markets. The recently announced 2026 China car of the year winner demonstrates this divide more clearly than ever before. An Audi model that carries a price tag equivalent to a basic A1 in France has claimed the top honor in the Chinese market. This recognition highlights the growing disparity in vehicle pricing and market positioning across different regions. The winning Audi model offers features and specifications that would typically command premium prices in European markets. Yet Chinese consumers can access this award-winning vehicle at a fraction of what European buyers pay for entry-level models. The price difference stems from several factors including local manufacturing partnerships and government incentives for domestic production. Chinese automotive policies have created an environment where international brands must adapt their pricing strategies to remain competitive. This approach has resulted in luxury vehicles becoming accessible to a broader segment of Chinese consumers. European buyers face a different reality when shopping for the same brand. A base model Audi A1 in France represents an entry point into the luxury segment with limited features & modest specifications. The contrast becomes striking when comparing what each market receives for similar financial investment. The award-winning Chinese market Audi includes advanced technology packages & premium materials as standard equipment. These features would require expensive optional packages in European configurations. The vehicle also benefits from newer platform technology and more efficient powertrains developed specifically for the Asian market. Manufacturing location plays a crucial role in this pricing equation. Vehicles produced within China avoid import tariffs and benefit from lower labor costs. Local production partnerships between Audi and Chinese manufacturers enable economies of scale that simply cannot exist for imported models in Europe. Consumer expectations differ significantly between these markets as well. Chinese buyers have grown accustomed to high levels of standard equipment and cutting-edge technology in their vehicles. Competition from domestic brands has pushed international manufacturers to offer more value to maintain market share. The French market operates under different constraints including stricter emissions regulations & higher taxation on vehicles. These factors contribute to elevated base prices even for entry-level luxury models. Also European consumers often accept lower standard equipment levels with the expectation of customizing vehicles through option packages. This growing gap raises questions about global brand positioning and value perception. Luxury manufacturers must balance their premium image in established markets while remaining competitive in rapidly growing Asian markets. The strategy that works in China may undermine brand prestige in Europe if consumers become aware of the disparities. The automotive landscape continues to shift as Chinese manufacturers gain technical capabilities and market influence. International brands face pressure to justify their premium positioning when local alternatives offer comparable quality at lower prices. This competitive environment benefits Chinese consumers but creates challenges for global pricing strategies. Looking forward the gap between markets may continue to widen. Chinese automotive policies favor local production and consumption while European regulations add costs to vehicle ownership. These diverging paths create distinct automotive ecosystems that operate under fundamentally different economic principles. The recognition of this Audi model as car of the year in China signals the maturity of that market. Chinese consumers and automotive journalists now evaluate vehicles using criteria that match or exceed international standards. The days of China being a dumping ground for outdated models have clearly ended. For European consumers this situation presents a frustrating reality. They pay premium prices for entry-level luxury vehicles while Chinese buyers access award-winning models at equivalent costs. The disparity seems difficult to justify from a pure value perspective. However the comparison oversimplifies complex market dynamics. Different regulatory environments & consumer preferences create unique conditions in each region. What succeeds in China may not translate directly to European tastes or requirements. The automotive industry stands at a crossroads regarding global pricing strategy. Manufacturers must decide whether to maintain regional price differences or move toward more unified global pricing. Each approach carries significant risks & potential rewards. This award and the discussion it generates reveal the changing balance of power in the global automotive market. China has evolved from a manufacturing base to a sophisticated market that drives innovation & sets trends. International brands must adapt to this new reality or risk losing relevance in the world’s largest automotive market. The gap between what Chinese and European consumers receive for their money will likely remain a contentious issue. As information flows freely across borders consumers increasingly question why such disparities exist. Manufacturers will need compelling explanations beyond simple market economics to maintain brand loyalty across regions.

➡️ “That’s typical of a bipolar person”: 6 signs psychologists spot immediately

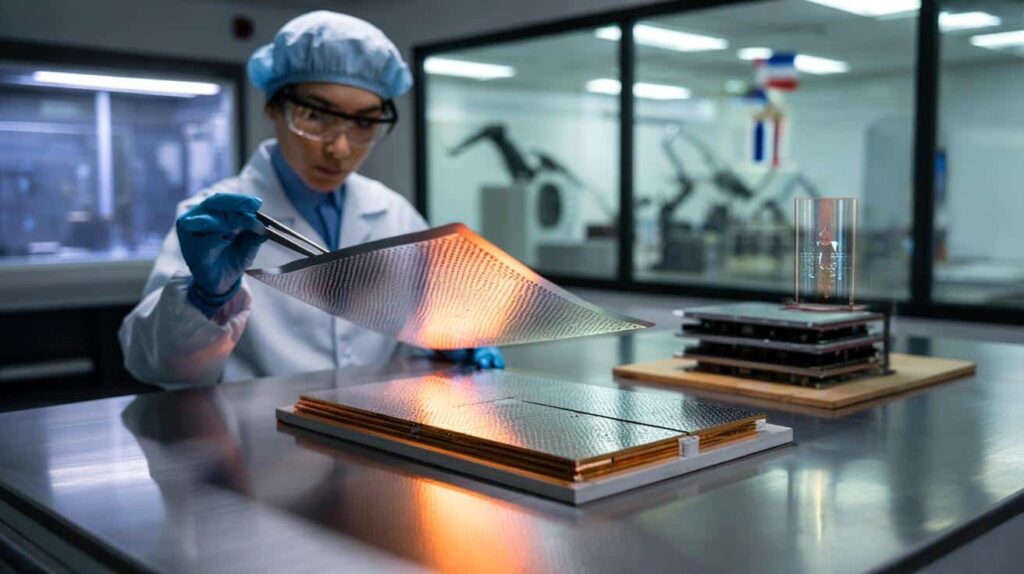

The French study that puts precise numbers on lithium thickness

Since 2022, a joint French project has been tackling this challenge head-on. It brings together the CEA (France’s public tech research powerhouse), Saft (a TotalEnergies subsidiary) and Automotive Cells Company (ACC, backed by Stellantis, Saft and Mercedes-Benz).

Their common goal: master ultra-thin lithium-metal negative electrodes and turn them into a process that can be industrialised. A new study from the project, published in 2025, goes beyond lab curiosity and sets clear reference points for industry.

For the first time, researchers outline a “sweet spot” thickness for lithium metal — between 20 and 50 micrometres — that balances performance, lifespan and manufacturability.

Evaporation instead of heavy metallurgy

Traditional rolling or calendering techniques struggle to produce uniform lithium foils thinner than about 20 micrometres at industrial scale. Surfaces become rough, mechanical defects appear, and quality control becomes a nightmare.

The French teams chose another route that looks more like microelectronics than metalworking: vapor deposition. Lithium is evaporated in vacuum and then condensed as a continuous film, usually on a copper foil that acts as a current collector.

At CEA Tech in Nouvelle-Aquitaine, researchers report dense lithium layers with low roughness and tightly controlled surface chemistry. Using advanced microscopy and nanometrology tools, they observe compact lithium grains and surfaces almost as smooth as the copper underneath.

That level of smoothness matters. Irregularities and contamination raise the risk of local hot spots, parasitic reactions and dendrite growth, all of which shorten battery life and threaten safety.

The “eroding landscape” analogy that clicked with engineers

The team then carried out a series of electrochemical tests on lithium layers ranging from 2 to 135 micrometres in thickness, initially in a liquid electrolyte setting to better understand degradation.

They identified three distinct regimes:

- Below 20 micrometres, there simply is not enough active lithium. Cells work at first, then fade quickly as the thin layer is consumed.

- Above 50 micrometres, more lithium does not bring more life. Interface resistance at the lithium–electrolyte boundary rises, and a lot of lithium is lost in irreversible side reactions.

- Between 20 and 50 micrometres lies a transition zone where lifetime and stability can still improve and design choices matter most.

Engineers behind the project describe the electrode like a piece of land under erosion. Too thin, and it vanishes rapidly under the “rain” of cycling. Too thick, and it builds up dead layers that choke the exchanges instead of protecting the soil. The viable path lies in this controlled middle ground.

Turning a lab breakthrough into an industrial playbook

For French industry, this is not just another scientific paper. It provides actual design targets and process tolerances. It confirms that ultra-thin, vapor-deposited lithium can be produced with the properties needed for solid-state batteries.

The study translates atomic-scale phenomena into thickness ranges and engineering rules that plant managers and equipment suppliers can use.

For Saft and ACC, the real question is not just: “Can we make it work?” It is also: “Can we make it at the right cost, with reasonable energy use, and with safety margins acceptable for cars, planes or defense systems?”

Using less lithium per cell cuts raw material demand and reduces exposure to price volatility and supply constraints. At the same time, thinner layers help maintain high energy density without increasing pack size.

Who is betting on solid-state in France?

A growing list of French and France-based players is moving from slide decks to hardware, patents and concrete factory projects. Together, they are building a local ecosystem around solid electrolytes, lithium metal and, in some cases, lithium-free alternatives.

| Group / consortium | Project status (2026) | Target technologies | Key partners |

| Argylium (Axens + Syensqo) | Pilot line in La Rochelle running; tonne-scale output aimed for 2027–28 | Sulfide solid electrolytes (around 500 Wh/kg, <10 min fast charge as target) | IFPEN, European carmakers |

| ACC (Stellantis, Saft, Mercedes) | Pilot cells; solid-state roadmap for 2028 and beyond | Polymer / sulfide solid electrolytes | Factorial (US), Solvay |

| Stellantis | Solid-state demonstrators validated by 2026 | Lithium metal with solid electrolyte | Factorial Energy (US) |

| Prologium France | Gigafactory under construction in Dunkirk | Ceramic solid-state lithium-metal cells (claiming 700+ Wh/kg) | Renault, French state |

| Torow | ASSB25 pilot project planned for 2027 | All-solid-state sodium batteries (no Li, Co or Ni) | DERBI-CEMATER cluster |

| E-lyt Labs | Pilot line expected operational in 2026 | Sulfide solid electrolytes with up to three times the volumetric energy of standard Li-ion | Automotive investors |

France’s battery manufacturing cluster holds important geopolitical significance. The country controls the entire production chain from electrolyte powders through to completed cells and pack integration. This comprehensive capability means France depends less on imports from Asia and retains more economic value within its own borders.

Beyond cars: where solid-state could hit first

While carmakers grab headlines, other sectors might adopt solid-state cells earlier, even at a premium price.

Aerospace and defense want safety and density

In aviation, every kilogram saved can cut fuel burn or unlock extra payload. High-energy solid-state packs with thin lithium metal could enable hybrid-electric aircraft, long-range drones or emergency power units where weight and safety both carry huge weight in certification.

Defense organizations pay close attention to this technology as well. Solid-state battery chemistries offer several important advantages including extended storage capability durability in harsh environments and the ability to withstand fire or ballistic impact.

Grid storage and “behind the meter” scenarios

Solid-state batteries offer better energy storage in smaller spaces on the power grid. This matters for crowded cities where there is not much room for storage equipment. These batteries could make it easier to install large systems on rooftops or in basements.

They might also pair well with intermittent renewables such as wind and solar, offering long service lifetimes and reduced maintenance for remote or critical sites.

What “solid electrolyte” and “lithium metal” really mean for users

For non-specialists, a few terms keep coming back.

# Solid Electrolyte

A solid electrolyte is a material that allows lithium ions to move through it while staying in a solid state. This material can take several different forms including ceramic, glass-like structures polymers or sulfide compounds. Each type of solid electrolyte comes with its own set of advantages and disadvantages when considering factors such as how well it conducts ions, how much it costs to produce, how stable it remains during use and how easy it is to manufacture at scale.

Lithium metal anode is a thin sheet of nearly pure lithium used as the negative electrode. Compared with graphite, it can store several times more lithium per gram, which directly boosts the energy of the cell. That gain is what justifies the effort around thickness control and interface engineering.

Silicon anodes could allow manufacturers to create smaller batteries that still deliver the same driving range. Alternatively they could keep battery sizes the same but offer vehicles that travel farther on a single charge and recharge more quickly. Another potential benefit is improved safety since these battery packs would be less likely to overheat & catch fire.

Risks, unknowns and realistic timelines

Despite the progress several risks still exist. Scaling up vapor deposition of lithium from small laboratory wafers to production levels of hundreds of thousands of square meters each year presents significant challenges. The success of this approach compared to traditional foil methods will depend on equipment costs and how efficiently the process can produce high-quality results at scale.

# Supply Challenges and Market Pressures

On the supply side improvements in lithium efficiency provide some relief. However, global demand continues to climb at a rapid rate. When recycling programs fail to match this growing need, the industry must turn to new mining operations. These projects often encounter significant environmental concerns & social opposition from local communities. Such resistance can disrupt supply chains & create price instability in the market. The gap between what recycling can provide and what manufacturers require puts pressure on mining companies to expand. Yet expansion brings its own set of problems that extend beyond simple economics.

Most French industrial plans now target the late 2020s for widespread use of solid-state batteries in regular electric vehicles. Before that happens these batteries will probably be tested first in specialized markets like luxury vehicles, aircraft military equipment and high-performance tools.

One realistic scenario sees hybrid architectures, where a car uses both conventional lithium-ion and a smaller solid-state pack, for example to handle fast-charging peaks or high-power bursts. This sort of combination could lower risk for manufacturers while they learn how new cells behave over a decade in real traffic.